How cannabis vape pens are reshaping flower sales, attracting younger consumers, and raising new health and safety questions.

For years, flower was the heart of cannabis culture. It still carries the ritual, the smell, the jar appeal, the connoisseur language, and the visual identity that built the category. But the numbers now show a major shift: vape pens are no longer a side product. They are becoming one of the most powerful forces in legal cannabis, pulling dollars away from flower, changing how younger consumers enter the market, and forcing producers to rethink what cannabis even looks like at retail.

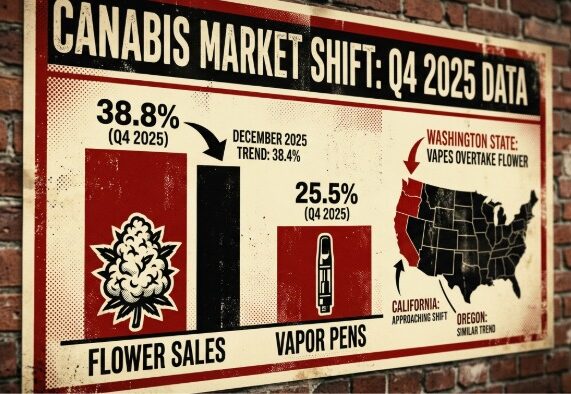

In the U.S. tracked by Headset, flower still leads category sales, but its share has been slipping while vapor pens hold a clear No. 2 position. By Q4 2025, flower accounted for 38.8% of U.S. cannabis sales and vapor pens 25.5%; through December 2025, flower fell to 38.4% while vapor pens stayed near recent highs at 25.5%. In Washington State, vapor pens have already overtaken flower as the top-selling category, and Headset says California and Oregon are getting close to that same crossover.

That matters because this is not just a product trend. It is a structural market shift. Headset’s 2026 report says both vapor pens and pre-rolls are steadily taking share from flower, especially in mature western markets, and that the shift is tied to convenience, ready-to-use formats, and younger consumer preference. Put simply: the industry is moving from “buy flower and prep it” to “buy something fast, portable, and discreet.”

Why younger consumers are leaning vape.

The clearest signal comes from age data. Headset reports that preference for vapor pens is strongly correlated with age, with Gen Z showing the highest affinity for the category. The firm argues that as that cohort ages deeper into the legal market, its preferences will increasingly shape product innovation and growth.

Federal survey data points in the same direction. The 2025 Monitoring the Future panel study found that among U.S. young adults ages 19 to 30, 22.3% reported vaping cannabis in the past year and 15.9% in the past 30 days in 2024, both the highest levels recorded since the measure was added in 2017. The same report found that past-year cannabis use among young adults was 41.4%, meaning vaping is not a niche behavior inside youth cannabis culture anymore — it is mainstream.

The age gradient continues beyond Gen Z, but it weakens as consumers get older. In the same survey, adults ages 35 to 50 reported much lower cannabis-vaping prevalence than young adults, and adults 55 to 65 were lower still. That does not mean older consumers are not buying vapes. It means the format is disproportionately strong with newer, younger, convenience-driven consumers.

Why vapes are so attractive

The answer is pretty obvious when you stop romanticizing it. Vapes are easy. No grinder, no rolling, no lighter, no ashtray, no strong lingering smoke, no glass, and less smell on your clothes. For a lot of consumers — especially apartment dwellers, younger professionals, and people who want a lower-profile experience — that matters more than tradition. This “ready-to-use” convenience is one of the biggest reasons vape pens keep gaining share.

There is also the design and product-format side. Headset found that category growth is increasingly concentrated in disposables, with 1g formats still dominant and larger formats like 2g showing momentum. That means the market is not only growing; it is being engineered toward convenience, portability, and value perception.

And then there is potency. Cannabis concentrates used in vape products can carry much higher THC concentrations than flower. NIDA notes that the risks of physical dependence and addiction increase with exposure to high concentrations of THC, and higher doses are more likely to produce anxiety, agitation, paranoia, and psychosis. That does not automatically make every vape worse than flower for every person, but it does help explain why some consumers see vapes as a stronger, faster, more efficient option.

What this means for the flower business.

Flower is not disappearing. It is still the largest category in the U.S. and in New York. But it is under pressure from both ends: pre-rolls on one side and vapes on the other. Headset describes this as a structural shift within inhalables, with ready-to-use formats gradually eroding flower’s dominance.

In New York, you can already see the tension. Headset’s February 2026 market data shows flower brought in about $57.67 million for the month, while vapor pens brought in $40.93 million. Flower is still ahead, but vapes are not far behind, and the vape category grew 42.0% year over year in the state.

At the same time, New York regulators have openly warned that flower is heading into a more competitive phase. In its 2024 market report, the Office of Cannabis Management said the state was seeing growing competitive pressure in flower, especially as indoor supply expands and pricing becomes a sharper weapon. OCM also noted that in mature markets flower prices have fallen more than 60% within five years of adult-use launch, driven by more cultivation capacity, better efficiency, and intense retail competition.

That is the business threat in plain English: if vapes keep capturing wallet share while flower prices keep compressing, flower producers may need to fight on quality, freshness, genetics, and storytelling — not just volume. Brands that can’t differentiate may get squeezed hard.

Who is producing the vape category?

Nationally, the vape market is fragmented by state, but some names repeatedly show up as category leaders or major multi-state players. Headset’s brand data shows brands like PAX and STIIIZY as important presences in vapor pens across multiple markets, while local and regional leaders dominate individual states.

In New York specifically, the current legal market has a clear set of vape players. Headset’s March 3, 2026 snapshot shows Jaunty dominating the state’s best-selling vapor-pen products, holding most of the top 10 SKUs. Separate Headset brand pages also show Jaunty ranked No. 1 in New York vapor pens from November 2025 through February 2026, with Ayrloom at No. 2, Fernway at No. 3, MFNY at No. 4, and Florist Farms holding the No. 6 position during that same stretch. New York Honey was outside the very top tier but climbed from 22nd to 15th in the same period, showing strong momentum.

That producer list matters because the vape race is not just about hardware. It is about extraction quality, oil formulation, flavor/terpene strategy, pricing, compliance, packaging, and trust. As the category grows, the brands that can combine consistency with legal-market credibility will likely have the advantage over flashy but less durable players. That is especially true in New York, where the legal market is still rapidly forming and consumers are learning who to trust.

Are vapes actually safer than smoking flower?

This is where the conversation gets messy.

The fairest answer is: they may reduce some combustion-related exposure, but they are not harmless, and the long-term science is still incomplete. The CDC says e-cigarette aerosol is not harmless “water vapor” and can contain harmful and potentially harmful substances. It also says aerosol generally contains fewer harmful chemicals than cigarette smoke, but that does not make vaping safe.

For cannabis specifically, the National Academies found substantial evidence that regular cannabis smoking is associated with airway injury, worse respiratory symptoms, and more frequent chronic bronchitis episodes. The same review noted a small feasibility study suggesting some respiratory symptoms may improve when people switch from smoking cannabis to using a vaporizer instead. But that is far from a blanket declaration that vaping is safe.

More recent research complicates the picture further. A 2020 JAMA Network Open study found cannabis vaping was associated with increased risk of bronchitic symptoms and wheeze in young adults. A 2025 respiratory review also reported that e-device users showed lower combustion-related metabolite levels than smokers, while still raising distinct respiratory and cardiovascular concerns and leaving long-term outcomes uncertain.

So the cleanest way to say it is this: smoking flower exposes users to combustion byproducts; vaping may lower some of that exposure, but it introduces aerosol-related risks, high-potency dosing issues, and contamination concerns.The science does not support “totally safe.” It barely supports “possibly less harmful in some ways.”

The contamination problem and the lesson from EVALI

Any serious vape investigation has to mention EVALI. CDC reported 2,807 hospitalized EVALI cases or deaths as of February 18, 2020, with 68 deaths confirmed. Investigations strongly linked the outbreak to vitamin E acetate in illicit THC vape products, especially products from informal or street sources. CDC’s guidance was blunt: people should not use THC-containing vaping products from informal sources and should not modify products or add substances not intended by the manufacturer.

That does not mean every regulated cannabis vape is comparable to the illicit products tied to EVALI. It does mean the category carries a unique trust problem: consumers are inhaling processed oil through a device, and any failure in testing, formulation, hardware, or sourcing can matter fast. Legal markets reduce some of that risk through testing and compliance, but they do not erase the broader health unknowns of inhaling heated oils and additives.

The economics: why retailers love vapes

Retailers love categories that are portable, shelf-efficient, fast-selling, branded, and repeat-purchase friendly. Vapes check a lot of those boxes. Headset notes that vapor pens remain the most expensive inhalable category, but also that pricing compression is making them relatively more affordable, which improves their competitive position against flower and pre-rolls.

In New York, average prices remain high across the market overall, but they are coming down as competition expands. Headset says New York’s average item price was $31.29 in February 2026, down from $35.41 a year earlier. Meanwhile, the broader market hit $163.5 million in February 2026, with the fastest year-over-year growth among large cannabis markets tracked by Headset.

New York’s OCM reported that combined adult-use and medical retail sales reached roughly $1.6 billion year-to-date in 2025, up from $1.0 billion in 2024 and $317 million in 2023. The agency also said the adult-use dispensary footprint grew from 261 stores in 2024 to 519 open dispensaries in 2025. More stores, more competition, more brands, and more pressure on prices is exactly the kind of environment where vapes can scale fast.

So are vapes “more trendy” than flower?

Among younger consumers, yes — clearly. In the broader market, not fully yet, but they are getting dangerously close in several states and have already crossed over in at least one mature market. The best way to put it is that flower still defines cannabis culture, but vapes increasingly define cannabis commerce.

That split is important. Flower still wins on ritual, authenticity, connoisseurship, and visual appeal. Vapes win on speed, stealth, portability, and format convenience. For older or enthusiast consumers, flower remains central. For younger consumers and many newer entrants, the vape is often the first choice — or the easiest one.

Bottom line

Vapes are not a fad. They are one of the biggest economic and cultural forces in legal cannabis right now. They are pulling share from flower, aligning strongly with younger consumers, rewarding brands that can execute extraction and hardware well, and forcing the industry to rethink how cannabis gets sold.

But the health story is far less settled than the sales story. Smoking flower carries known combustion-related risks. Vaping may reduce some of those exposures, but it is not harmless, long-term evidence remains incomplete, and the category has already lived through a major contamination crisis tied to illicit THC products. Higher-potency oils also raise separate concerns around dependence, dosing, and overuse.

The smart conclusion is not “vapes are safer” or “flower is dead.” It is this: vapes are winning the market battle, but the public-health verdict is still unfinished.